Introduction

The automotive interior materials market has emerged as one of the most dynamic and innovative segments of the global automotive industry. These materials, which include plastics, leather, textiles, metals, and composites, are essential for designing and manufacturing vehicle interiors that balance comfort, functionality, and aesthetics. With the rapid evolution of automotive technologies, changing consumer preferences, and rising demand for sustainable and luxurious interiors, this market is undergoing a significant transformation.

Globally, automakers are focusing on enhancing passenger experience while optimizing weight, safety, and sustainability. Interior materials play a pivotal role in improving fuel efficiency, reducing carbon emissions, and delivering superior tactile appeal. The market’s growth is being shaped by trends such as electric vehicle (EV) adoption, connected mobility, and smart cabin designs.

This report provides a detailed analysis of the global automotive interior materials market, exploring its current landscape, growth potential, challenges, and future opportunities. It highlights key market dynamics, competitive developments, and regional insights, offering valuable intelligence for manufacturers, investors, and industry stakeholders.

Source - https://www.databridgemarketresearch.com/reports/global-automotive-interior-materials-market

Market Overview

The automotive interior materials market encompasses the production and utilization of materials used in the interior cabin of vehicles—including seats, dashboards, door panels, headliners, and flooring. These materials determine the overall quality, comfort, and durability of vehicle interiors.

Historically, the market relied heavily on leather and conventional plastics. However, environmental concerns, technological progress, and changing consumer expectations have accelerated the shift toward lightweight, eco-friendly, and high-performance materials. The current market includes a wide array of materials such as thermoplastic polymers, polyurethane foam, synthetic leather, fabric, and bio-based composites.

Over the past decade, the automotive interior materials market has grown steadily, supported by rising automobile production, increased disposable incomes, and heightened emphasis on vehicle aesthetics and comfort. The rise of EVs and hybrid vehicles has also driven new interior designs focusing on minimalism, advanced infotainment systems, and sustainable material use.

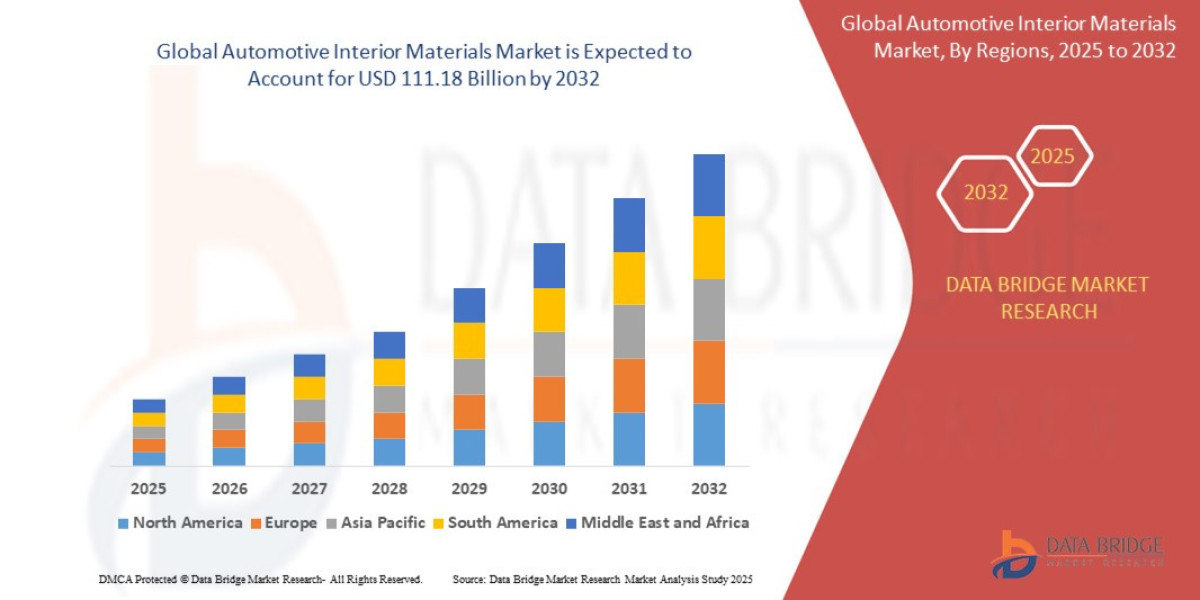

Regions such as Asia-Pacific and Europe dominate global production and consumption, with countries like China, Germany, Japan, and the U.S. leading technological innovation. As manufacturers adopt lightweight solutions to meet stringent emission standards, the market is expected to continue expanding at a healthy pace.

Market Drivers and Opportunities

Several key factors are propelling growth in the automotive interior materials market, creating opportunities for innovation and investment across the value chain.

1. Rising Demand for Comfort and Customization:

Modern consumers expect more than just performance—they seek premium, comfortable, and customizable vehicle interiors. Automakers are responding with high-quality materials that offer durability, sound insulation, and tactile luxury. This growing focus on passenger experience is a major catalyst for market expansion.

2. Sustainable and Eco-Friendly Materials:

Environmental concerns and regulatory pressures are driving the adoption of recyclable and bio-based materials. Many manufacturers are incorporating eco-friendly alternatives such as organic fabrics, recycled plastics, and plant-based leathers to reduce their carbon footprint. This transition toward sustainable materials aligns with the broader global push for green mobility.

3. Lightweighting for Fuel Efficiency:

The automotive industry’s shift toward lightweight vehicles to improve fuel efficiency and reduce emissions is another key driver. Advanced polymers, carbon-fiber composites, and other lightweight materials are replacing heavier traditional components, leading to both performance and sustainability benefits.

4. Growth of Electric and Autonomous Vehicles:

EVs and autonomous vehicles are revolutionizing automotive design. Interior materials are being reimagined to support new cabin layouts, infotainment systems, and advanced comfort features. The emphasis on acoustics, temperature control, and user-friendly interfaces creates fresh opportunities for material suppliers.

5. Technological Innovation and Smart Interiors:

Integration of digital technology—such as touch sensors, ambient lighting, and smart fabrics—is shaping the next generation of automotive interiors. Manufacturers are experimenting with materials that enhance interactivity, energy efficiency, and user engagement.

Together, these trends are driving substantial opportunities for suppliers to innovate in design, performance, and sustainability, making interior materials a cornerstone of automotive differentiation.

Market Challenges and Restraints

Despite its growth potential, the automotive interior materials market faces several challenges that could constrain expansion if not addressed strategically.

1. Volatile Raw Material Prices:

The fluctuating costs of petroleum-based products and other raw materials significantly impact production expenses. Manufacturers must constantly balance quality, performance, and cost efficiency while adapting to unpredictable price changes.

2. Stringent Environmental Regulations:

While sustainability initiatives offer opportunities, they also impose compliance challenges. Global regulations related to emissions, recycling, and material toxicity require continuous adaptation and innovation, increasing production complexity and cost.

3. Supply Chain Disruptions:

Geopolitical tensions, logistics bottlenecks, and shortages of key materials—such as resins and synthetic fibers—can disrupt production schedules and impact pricing. COVID-19 further exposed vulnerabilities in global supply chains, prompting companies to re-evaluate sourcing strategies.

4. High R&D and Tooling Costs:

Developing advanced materials and integrating new technologies requires substantial investment in research, testing, and manufacturing infrastructure. Smaller manufacturers often struggle to keep pace with larger competitors in terms of innovation and scalability.

5. Competition from Alternative Materials:

As new materials enter the market, existing ones face competitive pressure. For instance, natural fibers and eco-leathers are replacing conventional leather and PVC, forcing traditional material suppliers to innovate rapidly.

These challenges necessitate strategic investments in research, sustainability, and collaboration across the automotive value chain to maintain market competitiveness.

Market Segmentation Analysis

The automotive interior materials market can be segmented based on material type, vehicle type, application, and region.

By Material Type

Leather (Natural and Synthetic): Synthetic leather dominates due to its cost-effectiveness, versatility, and ethical advantages over natural leather.

Plastics: Widely used for dashboards, trims, and panels due to their lightweight and design flexibility.

Fabrics and Textiles: Popular for seats and headliners, with increasing use of sustainable fibers.

Metals and Composites: Applied in luxury vehicles for aesthetic appeal and structural integrity.

By Vehicle Type

Passenger Cars: The largest segment, driven by high consumer demand for comfort and aesthetics.

Commercial Vehicles: Focused on durability and low maintenance materials.

Electric Vehicles: Rapidly growing, emphasizing modern, minimalist, and sustainable interior materials.

By Application

Key applications include dashboard, seats, door panels, floor coverings, headliners, and trims. Seats and dashboards account for the largest share due to their direct impact on comfort and aesthetics.

By Regional Insights

Asia-Pacific: The dominant market, driven by robust automobile production in China, India, Japan, and South Korea. Rapid urbanization and economic growth continue to boost demand.

Europe: Strong focus on sustainability and premium vehicles. Germany and France lead innovation in eco-friendly materials.

North America: Driven by luxury car demand and advancements in EV interiors.

Latin America and the Middle East: Emerging markets with increasing adoption of modern automotive technologies and materials.

Overall, passenger vehicles and Asia-Pacific remain the most influential segments shaping market performance.

Competitive Landscape

The global automotive interior materials market is characterized by intense competition among multinational corporations and specialized material suppliers. Companies are focusing on technological innovation, strategic alliances, and sustainable material development to strengthen market presence.

Leading market players include Adient plc, Lear Corporation, Faurecia, Toyota Boshoku Corporation, BASF SE, Covestro AG, Continental AG, and Sage Automotive Interiors. These companies invest heavily in R&D to produce materials that balance performance, durability, and environmental sustainability.

Recent years have witnessed several mergers, acquisitions, and strategic partnerships aimed at expanding production capacity and technological capabilities. For example, partnerships between material science firms and automotive OEMs are accelerating innovation in lightweight composites and bio-based polymers.

Additionally, many suppliers are adopting digital manufacturing technologies such as 3D printing and AI-driven design to enhance customization and reduce production lead times. The focus is shifting toward circular economy models, where recycled materials are reintegrated into production, minimizing waste and carbon emissions.

Sustainability, innovation, and strategic collaboration are now the key differentiators for companies seeking competitive advantage in this evolving market.

Future Outlook and Trends

The automotive interior materials market is poised for strong growth over the next decade as automakers transition toward electrification, digitalization, and sustainability. Several trends are expected to shape its future trajectory.

1. Sustainable Material Revolution:

The industry will see a major shift toward renewable and recyclable materials, including natural fibers, bio-based polymers, and water-based adhesives. Automakers will increasingly integrate circular economy principles into their supply chains.

2. Smart and Connected Interiors:

Future vehicle cabins will become intelligent environments, featuring smart fabrics, haptic feedback surfaces, and integrated ambient technologies. These innovations will enhance comfort, safety, and interactivity.

3. Personalization and Luxury Demand:

Consumer demand for bespoke interiors will continue to grow. Luxury automakers are offering customizable options with premium finishes, driving demand for advanced materials that combine performance with aesthetics.

4. Growth of Electric and Autonomous Vehicles:

EVs and self-driving cars will redefine interior design, focusing on space optimization, acoustic insulation, and advanced ergonomics. This will create demand for innovative materials that support modular and reconfigurable cabin layouts.

5. Regional Expansion in Emerging Markets:

Developing economies in Asia, the Middle East, and Africa will see increasing vehicle production and consumer spending, offering significant growth opportunities for material manufacturers and suppliers.

As sustainability, technology, and user experience converge, the future of automotive interior materials will be defined by innovation, adaptability, and environmental responsibility.

Conclusion

The automotive interior materials market stands at the forefront of innovation in the global automotive sector. It combines design, technology, and sustainability to redefine the driving experience for modern consumers. Growing emphasis on lightweight, eco-friendly, and high-performance materials is transforming the way automakers approach vehicle interiors.

While challenges such as raw material volatility and regulatory constraints persist, the market’s long-term prospects remain strong. As electric mobility and smart interiors continue to evolve, material suppliers that prioritize sustainability and technological innovation will be best positioned for success.

The future of this market lies in creating interiors that are not only functional and luxurious but also environmentally responsible—representing a true fusion of performance and sustainability.

Frequently Asked Questions (FAQ)

What is the current size of the automotive interior materials market?

The market continues to expand steadily, driven by rising automobile production and growing consumer preference for comfort and sustainability. Asia-Pacific leads in production, while Europe remains a hub for innovation in eco-friendly materials.

What are the key drivers influencing growth in this market?

Major drivers include increasing demand for premium interiors, sustainability initiatives, growth in electric vehicles, and advancements in lightweight and smart materials.

Which regions dominate the automotive interior materials market?

Asia-Pacific dominates the market due to large-scale automotive manufacturing, while Europe and North America contribute significantly through innovation and high-end vehicle production.

Who are the major players in the industry?

Leading companies include Adient, Lear Corporation, Faurecia, BASF, Covestro, and Toyota Boshoku, all of which focus on advanced materials, strategic partnerships, and sustainability.

What are the latest trends shaping the future of this market?

Trends include the adoption of smart materials, eco-friendly solutions, 3D printing, and increased use of recycled and bio-based components in vehicle interiors.

What challenges could slow down growth in this sector?

Challenges include volatile raw material prices, environmental regulations, supply chain disruptions, and high research and development costs for innovative materials.

How can businesses benefit from investing in the automotive interior materials market?

Businesses can capitalize on growing demand for sustainable, premium, and technologically advanced interiors by investing in innovation, circular production, and strategic collaborations with automakers.

Global Hummus Market

Global Hypertension Management Devices Market

Global Industrial Metrology Market

Global Lab Automation Market

Global Life Science Instrumentation Market

Global Liquid Analytical Instrument Market

Global Medical Imaging Phantoms Market

Global Methylene Diphenyl Di-Isocyanate (MDI) Market

Global Microfluidics Market

Global Military Robots Market

Global Mixed Xylene Market

Global Mobile Value Added Services (VAS) Market

Global Network-as-a-Service (NaaS) Market

Global Neurovascular Embolization Devices Market

Global Nitrogen-Fixing Biofertilizers Market

Global Omega 3 for Food Ingredients Market

Global Optical Coherence Tomography (OCT) Market

Global Organic Cosmetics Market

Global Organic Honey Market

Global Paper Shredder Market

Browse More Reports:

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com